Trade Wars 2.0 Update

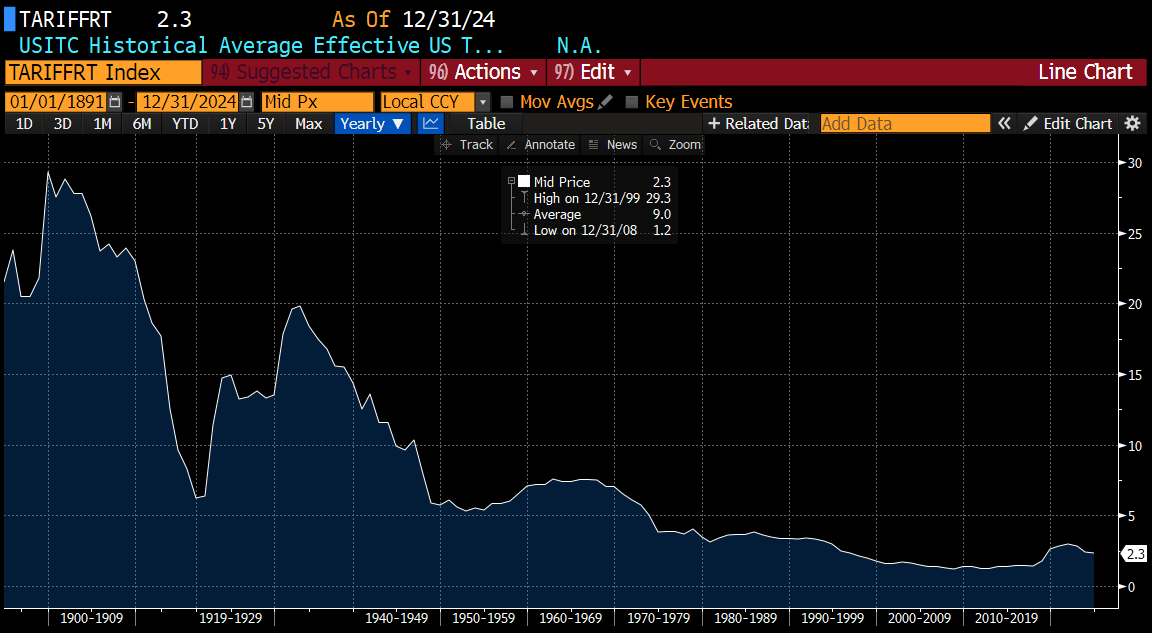

On April 2nd, the Trump administration announced reciprocal tariffs against countries that had existing tariffs on the United States. In addition, they added a minimum tariff rate of 10% on all US imports. The rate of the tariffs varied by country, but some of our largest trading partners included a 54% tariff rate on China, a 20% tariff rate on the EU, and a 32% tariff rate on imports from Taiwan. The full list is included below, but if implemented, it brings the overall effective tariff rate to 25%, a sizeable increase from 2.3% at year-end. The last time the effective US tariff rate exceeded 20% was in 1911. From a tax revenue perspective, it would raise around $400 billion in tax revenue and would be the largest tax increase since the Revenue Act of 1968. Overnight, markets responded to the announcement by immediately selling off, with the S&P 500 futures down over 3%.

US Historical Average Tariff Rate Since 1891. Source: Bloomberg

What’s Next?

The tariffs will be implemented effective Saturday, April 5th, so there are several days before they go into effect. Secretary Bessent told Bloomberg News that should countries not retaliate against their tariff rates, these rates will stay where they are. If other countries do retaliate, it appears the administration is willing to increase these rates. The EU has an emergency meeting on April 3rd to discuss retaliation. Japan, China, South Korea, and Vietnam have all said they will raise tariffs together against the US in the event these reciprocal tariffs are implemented. Markets will be keenly focused on how these countries respond in the coming days.

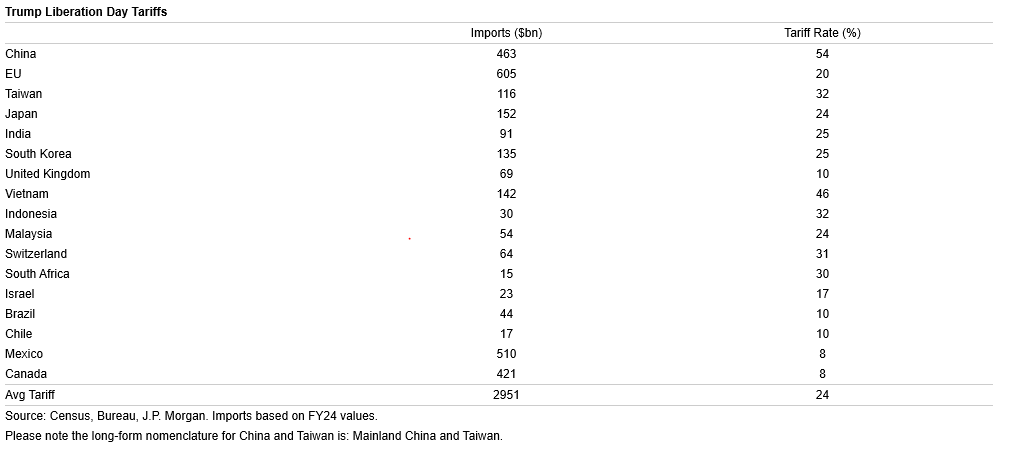

Liberation Day Tariffs By Country. Source: JPMorgan

The Full Impact

If the tariffs are implemented over time at these levels, economists are predicting that the US and global economy could enter a recession by year-end. The expectation is that the US economy could be negatively impacted by 2 percentage points of GDP while inflation could rise several percentage points. For US consumers, it will likely cause prices to rise in the coming weeks in addition to causing supply chain issues. For companies, earnings will likely be negatively impacted as costs rise. The S&P 500 still trades at 21x forward earnings, well above the 10-year historical average of 17x. Additionally, analyst consensus earnings growth for the S&P 500 this quarter is 18%, a high bar. Any negative impact on earnings growth should push stock prices lower. We are entering 2Q earnings season, so analysts will keenly focus on management Q&A during earnings calls for any potential tariff or trade impact. From a global perspective, central banks should likely start to look to lower rates, particularly the ECB. In Asia, China is fixing the yuan in a way that is significantly increasing the risk that they will intervene in currency markets.

How Are We Responding?

Within our asset allocations, we continue to maintain a relative underweight to US equities versus our strategic targets. In addition, we are overweight fixed income and cash which should reduce portfolio volatility as well as provide some “dry powder” should we get a tariff headline that may cause a reversal in the risk-off sentiment. We also have an allocation to gold as an alternative to hedge any inflation or macro risk from rising inflation and trade uncertainty. Within our equity strategies, we have a higher-than-normal allocation to cash from trimming exposure to companies that could be more exposed to international trade and tariffs. Over the last several months, we increased exposure to higher-quality companies with stronger and more durable balance sheets and earnings potential that could outperform it’s peers in a slowing growth environment.

Moving forward, regardless of which direction the markets head, given the day-to-day headline risk, volatility will remain elevated, and we will continue to “play defense” until we get more clarity.